VAT Reverse Charge

What Is The VAT Domestic Reverse Charge For Building & Construction Services?

HMRC introduced the VAT domestic reverse charge for building and construction services which was going to apply from 1 October 2019 and has published Guidance Notes. However, the industry simply was not ready and undoubtedly there would have been problems with the new system.

This scheme, which defines the treatment of VAT during specific business-to-business service supplies, was originally due to launch on 1 October 2019 but was delayed by one year to 1 October 2020, before it was further delayed by another five months to 1 March 2021 due to the impact of coronavirus.

Our expert Consultants can help explain the new rules and provide further detailed guidance on how the VAT domestic reverse charge for building and construction will affect your cash flow and what you can do about it.

The new VAT reverse charge rules will definitely impact all Specialist Contractors, Trade Contractors and Subcontractors, so if you have a problem please call our friendly team and speak to one of our expert Consultants on 01773 712116 or email info@streetwisesubbie.com. You will not be charged unless you decide to appoint one of our Consultants to act on your behalf.

The domestic reverse charge will be introduced without a transitional period and will have a significant impact on the accounting practices and cash flow of businesses in the construction sector.

VAT Reverse Charge For Building and Construction Background

The aim of this measure is to combat missing trader fraud in the construction sector in a similar way to the previously introduced domestic reverse charges for the sale of computer chips and mobile phones.

Under the new regime, VAT-registered Specialist Contractors, Trade Contractors and Subcontractors who supply certain construction services to another VAT-registered business (e.g. a Main Contractor or another subcontractor) for onward sale, will be required to issue a VAT invoice stating that the service is subject to the domestic reverse charge.

The recipient of those services must then account to HMRC for the VAT due on that supply through its VAT return, instead of paying the VAT amount to the Specialist Contractor, Trade Contractor or Subcontractor. The recipient can then recover that VAT amount as input tax, subject to the normal rules.

Which Services Will VAT Reverse Charge Apply To?

The new domestic reverse charge will apply to supplies of ‘specified services’ between VAT registered businesses where the recipient then makes an onward supply of those specified services.

It applies to the following building and construction services at either standard or reduced rate VAT:

- Construction, alteration, repair, extension, demolition or dismantling of buildings or structures (whether permanent or not), including offshore installations.

- Construction, alteration, repair, extension or demolition of any works forming, or to form, part of the land, including (in particular) walls, roadworks, power-lines, electronic communications apparatus, aircraft runways, docks and harbours, railways, inland waterways, pipe-lines, reservoirs, water-mains, wells, sewers, industrial plant and installations for purposes of land drainage, coast protection or defence.

- Installation in any building or structure of systems of heating, lighting, air-conditioning, ventilation, power supply, drainage, sanitation, water supply or fire protection.

- Internal cleaning of buildings and structures, so far as carried out in the course of their construction, alteration, repair, extension or restoration.

- Painting or decorating the internal or external surfaces of any building or structure.

It also applies to services which form an integral part of, or are preparatory to, or are for rendering complete, the services described in the bullet points above including site clearance, earth-moving excavation, tunnelling and boring, laying of foundations, erection of scaffolding, site restoration, landscaping and the provision of roadways and other access works.

The legislation is designed so that if there is a reverse charge element in a supply then the whole supply will be subject to the domestic reverse charge.

Where specified services have been provided then subsequent services on the same site by the same supplier may also be covered by the domestic reverse charge, if both parties agree.

This has been introduced to speed up the decision-making process on whether the domestic reverse charge should apply.

However, where the original services did not come within scope of the domestic reverse charge, but subsequent services do, then the VAT treatment changes. Businesses will need to review and monitor the VAT position throughout a project.

Which Services Are Excluded In VAT Reverse Charge?

The domestic reverse charge will apply to specified services unless:

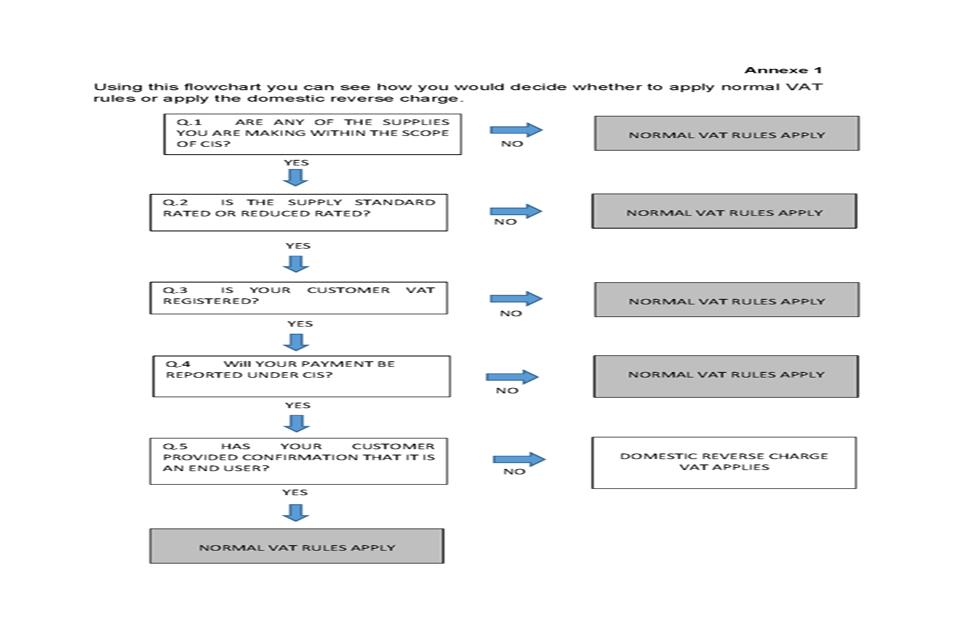

- The services are supplied to an end user, such as the property owner, or directly to a main contractor that sells or lets a newly completed building.

- The recipient makes onward supplies of those construction services to a connected company.

- The recipient is not VAT registered, or required to be VAT registered.

- The recipient is not registered for the CIS.

- The supplier and recipient are landlord and tenant or vice versa, or

- The supplies are zero-rated.

An end user is a person who receives the specified services for any purpose other than making an onward supply of those services. Where the customer has not provided confirmation that it is an end user either in writing, an email, or in the contract, HMRC’s guidance is that the supply will come within the scope of the domestic reverse charge and no VAT is charged.

However, on occasions it will be clear to the Specialist Contractor, Trade Contractor or Subcontractor that its customer is an end user and should be charged VAT but the customer has not given confirmation. In these cases, HMRC’s latest guidance says that it will be acceptable to charge VAT in the normal way.

In addition to confirming if your customer is an end user you should also require them to confirm their VAT and CIS status and provide their VAT number. We would recommend that this is confirmed in the contract before any invoices need to be raised.

Where goods and building materials are provided together with construction services and in the course of the construction work then the reverse charge also applies to these goods.

VAT Reverse Charge Invoices

Invoices for services subject to the domestic reverse charge must include all the information required on a normal VAT invoice. However, they must make it clear that the domestic reverse charge applies and that the customer is required to account for the VAT. There is no specific wording but HMRC provide examples of suitable wording: “Reverse charge: VAT Act 1994 Section 55A applies” “Reverse charge: S55 VATA 94 applies” “Reverse charge: Customer to pay VAT to HMRC”.

Where customers issue authenticated tax receipts or self-billing invoices HMRC’s recommended wording is: “Reverse charge: we will account for and pay the output tax due to HMRC” “Reverse charge: as the UK Customer we will pay the VAT due to HMRC”.

Impact Of VAT Reverse Charge On Specialist Contractors, Trade Contractors & Subcontractors

The implications for you and your cash flow:

- You will still be paying VAT to your suppliers and some subcontractors but NOT collecting it from the Contractor.

- Your cash flow will be hit until the end of each VAT accounting period.

- You will no longer be able to rely on VAT money for cashflow.

- The onus will fall on major Contractors to pay very large sums of money to the exchequer.

- Ensure your accounting systems are capable of processing reverse charge supplies.

- The whole of industry will need to get to grips with a new accounting system, or risk being mired in complex red tape.

- The potential for confusion and manipulation is enormous

VAT Reverse Charge – What Action Should You Take?

- Ensure you fully understand the new arrangements – see seminar details below.

- Review supplies made to and received from other VAT registered contractors to establish where these will be subject to a reverse charge from October 2019.

- Check any guidance supplied by the Main Contractor with whom you are in contract.

- Where necessary obtain notification from customers that they are an end user and confirmation of their VAT registration and CIS status.

- Consider any adaptions required to ensure accounting systems can deal with this change and,

- Consider the impact on cash flow from October 2019 and if there are any other ways to mitigate this.

Construction VAT Reverse Charge Problems?

If you have any kind of problem with the VAT reverse charge for building and construction services, it is definitely worth getting some professional advice sooner rather than later.

Help With VAT Domestic Reverse Charge For Building and Construction

Why not use the Ask Streetwise feature on this site to ask our team of expert Consultants for help if you have a problem relating to the payment of VAT on construction services?

Or simply give us a call and speak directly to one of our expert Consultants for Free initial advice on 01773 712116 or email: info@streetwisesubbie.com. You will not be charged unless you decide to appoint one of our Consultants to act for you.

Really Useful Articles On VAT Domestic Reverse Charge For Building and Construction

“Design and billed: reverse charge VAT explained” by Natwest

What is the expected impact of reverse charge VAT on the construction industry?

- From 1 October, ‘reverse charge’ VAT will be introduced in the construction industry, stopping traders from charging VAT to their customers, who will account for the tax themselves instead

- Designed to prevent ‘missing trader fraud’, the change could see subcontractors lose a sizeable share of working capital

- With research suggesting the industry is poorly prepared, trade associations are urging the government to delay implementation

On 1 October 2019 [now postponed to 2020], the way VAT is collected from most contractors and subcontractors in the building and construction industry is due to change. But with many small businesses believed to be unaware of the introduction of ‘reverse charge’ VAT, the sector is being urged to prepare.

The reverse charge is designed to stop missing trader fraud, in which a trader charges VAT on a service, but absconds before passing the VAT on to HMRC. This type of fraud is thought to cost the Treasury tens of millions of pounds every year.

The reverse charge prevents it by stopping the trader – in this case usually a subcontractor – charging VAT to their customer, usually another contractor who hired them. Instead, the customer accounts for the VAT themselves. Similar reverse charges have proved successful in other sectors, including wholesale telecommunications, gas and electricity.

The charge will apply to most businesses or sole traders in the industry that are registered for VAT, including those using the Construction Industry Scheme (CIS), under which contractors in the industry must deduct money from subcontractors’ payments and pass it on to HMRC. There are some exemptions, including for work related to mineral or gas extraction, the manufacture of equipment used in construction, and installation of security systems. Architects, surveyors and most employment businesses supplying construction workers will also be exempt.

The charge is not applicable if a service is provided to an ‘end user’: someone using the services themselves, rather than selling them on as part of their own service package. Landlords and tenants are treated as end users.

Pressure on margins

Raphael Suissa, VAT adviser at accountancy firm BKL, describes how the new rules might affect a building renovation project in which a contractor hired plumbing and electrical subcontractors to complete £100,000 worth of work. Previously, the subcontractors would have issued invoices for £120,000, including VAT.

“Following the change, the subcontractors will invoice the contractor for £100,000. They will have a statement on their invoice saying that these services are subject to the reverse charge, and they will tell the contractor how much VAT they are liable for,” Suissa explains. “The contractor will account for this reverse charge on their VAT return. The contractor will not be out of pocket, but the subcontractor will have to manage without the £20,000 they would have been paid in VAT, which they may previously have used – legitimately – as working capital.”

This is the biggest problem. “Most people that will be affected by this are working in small and medium-sized businesses, operating on quite tight margins,” says Richard Dalton, tax partner at professional services firm BDO. “How do you manage a reduction in your working capital that equates to 20% of turnover?”

Mitigating steps and potential pitfalls

There are some ways they might soften the blow. Contractors or subcontractors who will now pay more VAT on purchases than is due to them for sales may wish to switch from quarterly to monthly VAT returns, giving them a more regular flow of cash from HMRC.

In theory, they could also negotiate better stage payments from the contractor paying them to help cash flow, but this could be difficult.

Otherwise, they may need to consider other sources of finance available from a bank or alternative lender, including invoice factoring or discounting services.

Larger contractors will escape significant cash-flow problems, but will have extra administrative duties, because they must check to see which transactions were subject to the reverse charge.

“Most people that will be affected by this are working in small and medium-sized businesses, operating on quite tight margins. How do you manage a reduction in your working capital that equates to 20% of turnover?”

“One potential pitfall for the mid-contractors or big contractors is if they have been charged VAT incorrectly and claim it back from HMRC,” says Daniel May, VAT specialist at MHA Larking Gowen chartered accountants. “The contractor’s only recourse will be for the supplier to resubmit the invoice. But the supplier might have gone bust, or be difficult to find.”

Other concerns relate to some of the complexities of the new regime, such as whether or not a customer can be classified as an end user or an ‘intermediary’, meaning the reverse charge would not apply. (Intermediaries are CIS- and VAT-registered businesses that are connected to the end user, through sharing an interest in the land where the construction is taking place, or being part of the same corporate group, for example.) If a subcontractor or contractor assumes the wrong status for a customer when invoicing them, the customer will be expected to notify the contractor and request a corrected invoice.

“This is where HMRC have complicated things,” says Veronica Donnelly, VAT partner at Campbell Dallas chartered accountants. “The subcontractor will have to ask.”

Still work to do

Like Dalton, Donnelly is worried that smaller firms could find it particularly difficult to prepare for the reverse charge. Their concerns are shared by the Federation of Master Builders (FMB). In July 2019 the trade association wrote to the Treasury warning that its research showed that more than two thirds of small businesses in the construction sector (69%) were unaware of the reverse charge. Even among those that did know about it, 67% had put no preparations in place for it.

The FMB also complained that HMRC had published guidance on the reverse charge only four months before it was due to come into effect; and that the guidance was not user-friendly.

With construction companies also having to deal with Brexit uncertainty, rising costs and skills shortages, the FMB called for a six-month delay to the introduction of the charge and improvements to the guidance.

Sarah McMonagle, director of communications at the FMB, says its stance has attracted support from other trade bodies, including the CBI and Build UK.

“Unless people know the change is coming, this could be very chaotic, especially for the smallest businesses,” says McMonagle. “We have tried to do our best in terms of spreading the message, but the very smallest companies are the hardest to reach.”

“I think their fears are justified,” says Donnelly. “I think HMRC has underestimated how much work there is to do.”

HMRC has said it will take a light-touch approach to enforcement for the first few months after October – but also that it will have little sympathy for firms that have failed to prepare.

“The important thing to do now is just to remind businesses to take this seriously,” says Donnelly. “They need to start preparations now. If they can’t do it themselves, they should seek help from advisers.”

How To Get Help With The VAT Domestic Reverse Charge For Building and Construction

Why not use the Ask Streetwise feature on this site to ask our team of expert Consultants for help if you have a problem relating to the payment of VAT on construction services?

Or simply give us a call and speak directly to one of our expert Consultants for Free initial advice on 01773 712116 or email: info@streetwisesubbie.com. You will not be charged unless you decide to appoint one of our Consultants to act for you.

Follow